What Is a Credit Score, Really?

A credit score is a three-digit number (ranging from 300 to 850) that reflects your creditworthiness. In other words: how likely you are to pay back what you borrow.

It’s based on your credit history, and lenders use it to decide whether to approve your mortgage—and what interest rate you’ll get. The higher the score, the better the deal.

But it’s not just about getting approved. A solid credit score can literally save you tens of thousands of dollars over the life of your loan.

What Makes Up Your Credit Score?

Here’s what goes into that magic number:

- Payment History (35%)

Are you paying bills on time? Lenders want consistency. One late payment can ding you more than you’d think. - Credit Utilization (30%)

This is how much credit you’re using compared to what’s available. Ideally, keep it under 30%. High balances = red flags. - Length of Credit History (15%)

The longer your credit accounts have been active, the better. Think of it like building trust over time. - Credit Mix (10%)

A mix of credit cards, auto loans, student loans, etc., shows you can juggle different types of debt responsibly. - New Credit Inquiries (10%)

Every time you apply for credit, it triggers a “hard inquiry.” Too many of these in a short span? Lenders get nervous.

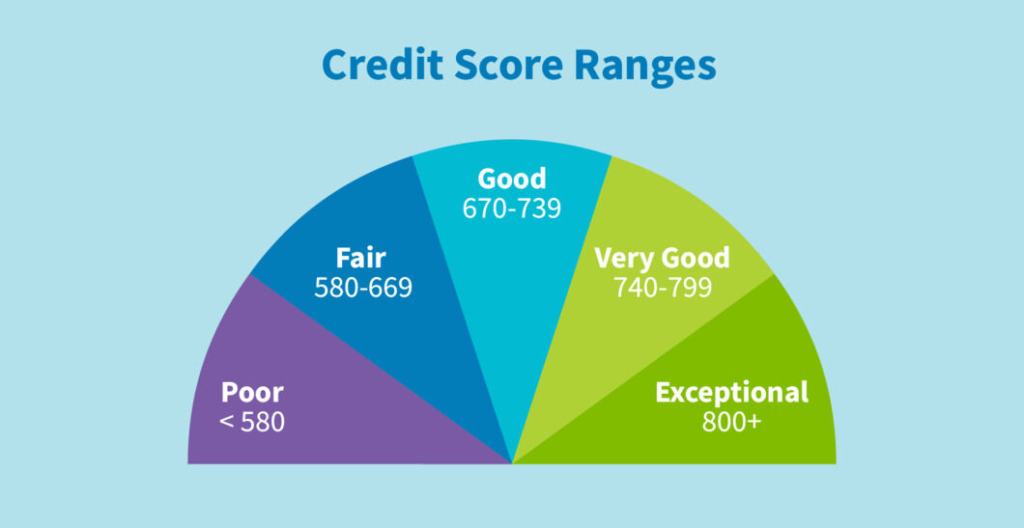

What Score Do You Need to Buy a House?

You don’t need a perfect 850. In fact, most buyers don’t even come close. Here’s a general guide:

- 580 – 620: You may qualify for FHA loans, but expect higher interest rates.

- 620 – 680: You’re in a better position for conventional loans.

- 680 – 740: Now we’re talking. You’ll likely land a solid rate and better terms.

- 740+: You’re in elite territory. Lenders will love you, and so will your wallet.

Pro tip: Even a 20-point jump in your score could mean the difference between a good rate and a great one.

Source: creditrepair

How to Improve Your Credit Score Before Buying

If your credit score isn’t where you want it to be yet, don’t stress—it’s fixable. Here’s where to start:

- Pay everything on time. No exceptions. Set up autopay if you need to.

- Pay down your credit cards. Focus on lowering your balances.

- Don’t open new credit lines unless you need to.

- Dispute errors on your credit report. You’d be surprised how often mistakes happen.

- Keep old accounts open. Even if you don’t use them—older accounts help boost your history.

Check Your Score—Before a Lender Does

Before a lender pulls your credit, do yourself a favor and check it yourself. You can get a free report from AnnualCreditReport.com, and most credit card companies offer a peek at your score, too.

✅ Yes, it’s safe and 100% legit.

AnnualCreditReport.com is the only site federally authorized by law under the Fair Credit Reporting Act (FCRA) to provide your free credit report. It’s backed by the Federal Trade Commission (FTC) and connects you directly to Equifax, Experian, and TransUnion—no middlemen, no strings attached.

⚠️ Just be careful: There are a lot of scammy lookalike sites out there. Make sure you’re on the real one: 👉 www.AnnualCreditReport.com

Final Thoughts: Your Credit Score Is Your Launchpad

Here’s the deal: Your credit score isn’t just a number—it’s a tool. A key. A launchpad into homeownership.

The good news? You don’t need to be a financial wizard to build strong credit—you just need a game plan, a little discipline, and the right people guiding you.

When you’re ready to take that next step, I’m here to help. Whether you’re buying your first home or your forever home, I’ll walk you through every step—credit score questions and all.

Let’s turn that dream into an address.

Ready to Make a Move?

If you’ve got questions about credit scores, pre-approvals, or just want to talk through your home buying strategy—I’ve got your back.

📞 Schedule your free homebuyer consultation today and let’s get you one step closer to your new front door.